Key Blockades of Input Tax Credit (ITC) under Section 17(5) of the CGST Act, 2017.

Summarizing the key blockades of Input Tax Credit (ITC) under Section 17(5) of the CGST Act, 2017.

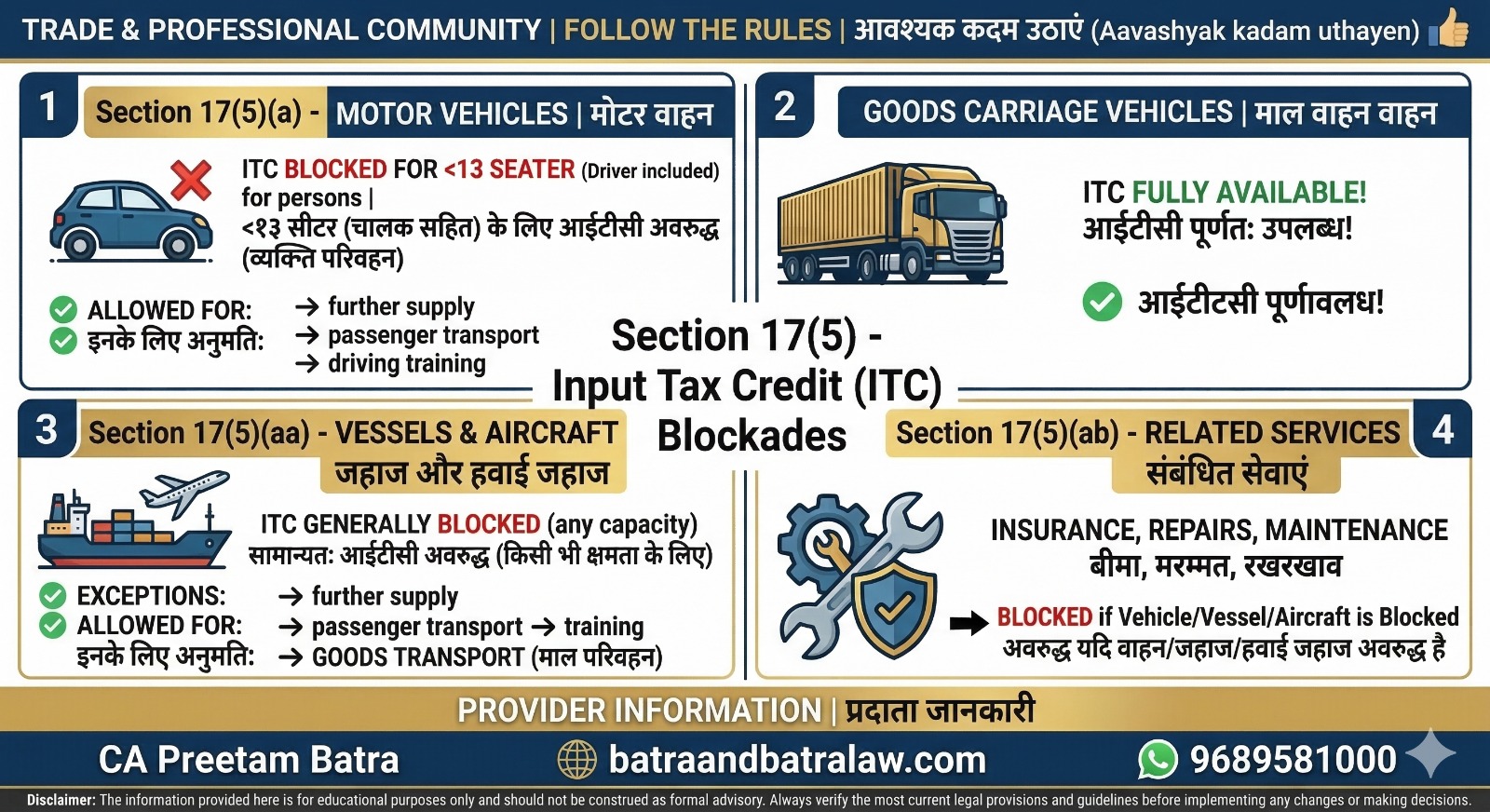

Key Highlights from the Article:Section 17(5)(a) -

Motor Vehicles: ITC is blocked for motor vehicles designed for transporting persons with a seating capacity of $\le$ 13 (including the driver).Exceptions: Credit is allowed if used for further supply, passenger transportation, or driving training.

Goods Carriage: ITC is fully available for vehicles meant for transporting goods.Section

17(5)(aa) - Vessels & Aircraft: ITC is generally blocked regardless of seating capacity.Exceptions: Allowed for further supply, passenger transport, training, or transportation of goods.Section

17(5)(ab) - Services: ITC on insurance, repairs, and maintenance is blocked if the underlying vehicle/vessel/aircraft is blocked.

Have Questions? We're Here to Help

Get expert advice from Batra & Batra Tax Insights. Reach out to discuss your requirements.